Malaysia: Pillar Two Implementation Expected in February 24 Budget

It is expected that the Pillar Two global minimum tax may be among the measures implemented in Budget 2023 on February 24, 2023.

Singapore To Implement Pillar Two From 2025

In the 2023 Budget Speech, the Singapore government announced it is to implement Pillar Two from 2025.

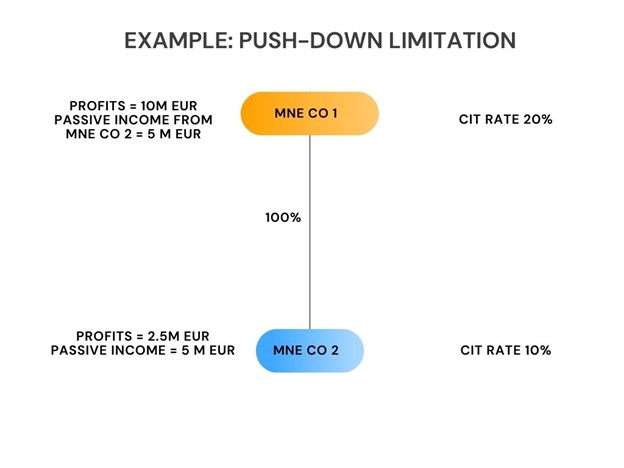

Treatment of CFC Taxes: QDMTTs vs GloBE Rules

Under Article 4.3.2(c) of the OECD Model Rules, tax paid under a CFC regime is generally allocated for GloBE purposes to the CFC entity. However, Article 5.1.3 of the OECD Administrative Guidance confirms that this is not the case for Qualified Domestic Minimum Top-Up Taxes (QDMTTs).

Pillar 2 Navigator Update for OECD Administrative Guidance: GloBE Adjustments

The Pillar Two Navigator – GloBE Adjustments chapter has been updated for the OECD Administrative Guidance.

Pillar Two Elections Updated For OECD Administrative Guidance

The OECD Administrative Guidance included a number of new elections available to MNEs to simplify or minimise some of the adverse impacts of the GloBE Rules. We have updated our Pillar Two Elections product to include all GloBE Elections.

Vietnam Needs to Act Fast After The South Korean Pillar Two Law

One of the tools to attract FDI to Vietnam is tax incentives. However, from the beginning of 2024, applying the Global Minimum Tax Rule at 15% will reduce Vietnam’s competitiveness. Although corporate income tax is currently at 20%, Vietnam applies a number of tax incentives.

The Equity Investment Inclusion Election

Article 2.9 of the OECD Administrative Guidance provides for an Equity Investment Inclusion Election. This relates, in part, to the interaction of Articles 3.2.1(c) and 4.1.3(a) of the OECD Model Rules.

Germany Confirms Pillar Two Law to be Gazetted in 2023

German Finance Minister Christian Lindner (FDP) has announced the presentation of a “tax fairness law” and a tax “growth package” for 2023. It was also confirmed the Law to implement the Pillar Two GloBE Rules will be gazetted in 2023.

Pillar 2 Navigator Update: Additional Top-Up Tax & Excess Negative Tax Expense Carry-Forwards

As an alternative to incurring additional top-up tax when a domestic tax loss exceeds the GloBE loss, Article 2.7 of the OECD Administrative Guidance provides that an MNE can elect for the Excess Negative Tax Expense administrative procedure.

Pillar 2 Navigator Update: Deferred Tax & Substitute Loss Carry Forwards

Article 2.8 of the OECD Administrative Guidance provides for the inclusion of deferred tax in the GloBE deferred tax adjustment amount for ‘Substitute Loss Carry Forwards’.