UAEs New Corporate Tax Law and Pillar Two

On 9 December 2022, the UAE issued the Federal Decree-Law No. (47) of 2022 on the taxation of corporations and businesses. In this article we look at the new UAE CT Law from a Pillar Two perspective.

Full Steam Ahead For EU Pillar Two Implementation

The EU Council has reached agreement on the implementation of Pillar Two. As Pillar Two gains momentum the critical mass of countries required for effective implementation gets closer.

Today’s OECD Consultation Document on Amount B of Pillar One

The OECD published a consultation document on Amount B of Pillar One today. We take an initial look at the key aspects of the Amount B consultation.

Thailand’s Tax Incentive Regime and Pillar Two

In this article, we take a look at Thailand’s tax regime from a Pillar Two perspective, with a particular focus on their tax incentives.

New Zealands Approach to Pillar Two

There are features of the NZ regime that raise issues from a Pillar Two perspective. Some of these were addressed in a Pillar Two consultation document issued earlier this year. In this article we look at some of the key issues in the implementation of Pillar Two for New Zealand.

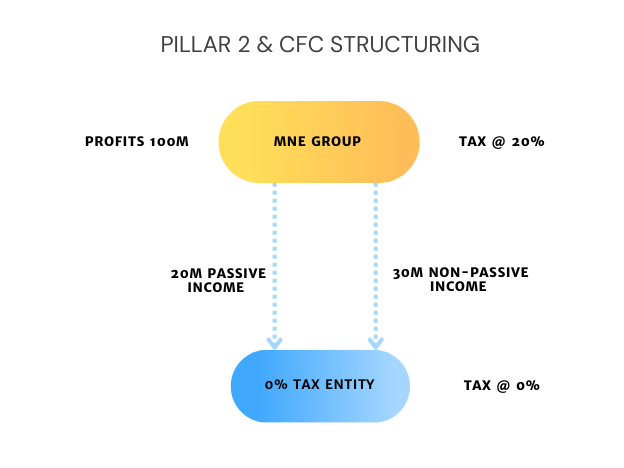

Profit Shifting to CFCs to Reduce Pillar 2 Top-Up Tax

Article 4.3.2(c) of the OECD Model Rules allocates tax paid on CFC income to the CFC entity (subject to a pushdown limitation). However, this leads to a situation where an MNE can reduce potential top-up tax by allocating more income to a CFC entity.

VAT on Digital Services Tracker: Updated

Our Global VAT on Digital Services Tracker has been updated and now covers over 80 jurisdictions.

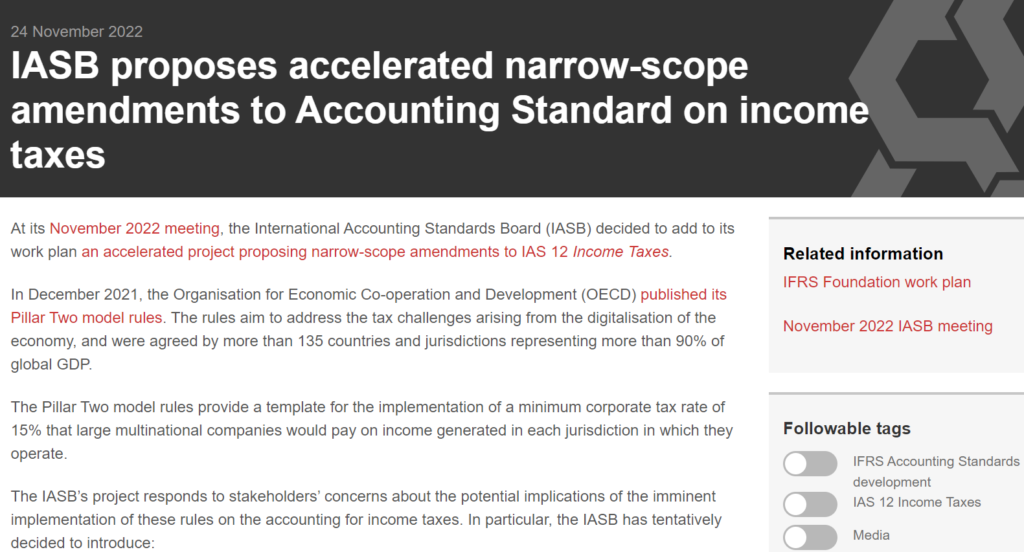

IASB Agrees to Amendments for Pillar Two Accounting

Whilst a number of the measures follow the proposals in the November Staff Paper, the prospect of certain other additional disclosures not previously suggested, has been put forward. In this article we review the IASB’s announcement and proposed changes.

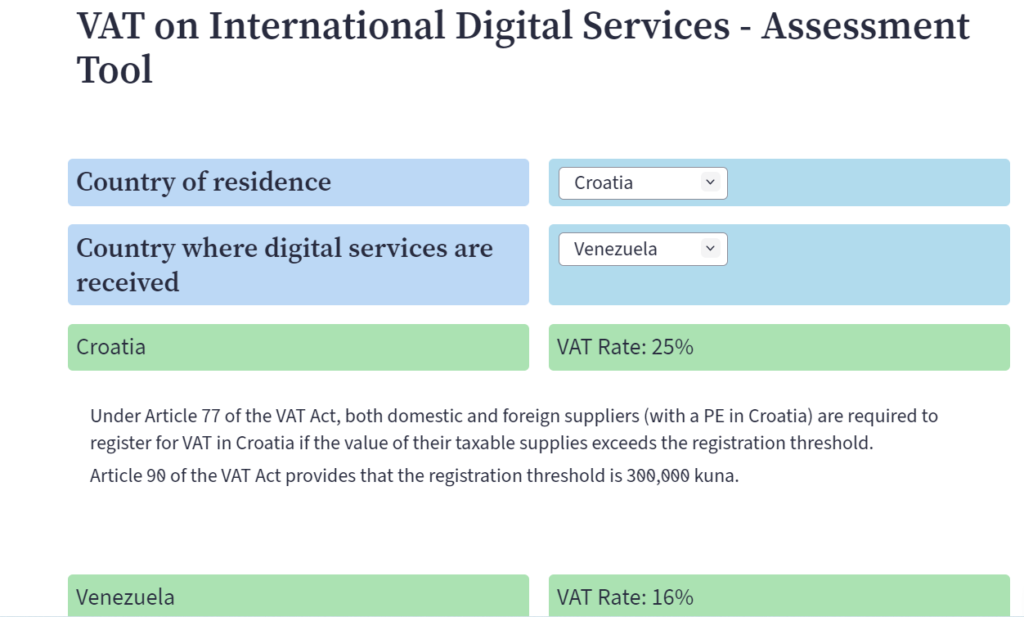

VAT on Digital Services: Global Assessment Tool

Use our global assessment tool to determine the VAT position on the provision of international digital services. The tool is fully cited to the relevant domestic law.

Luxembourg Private Debt Funds and Pillar Two

Luxembourg is home to the second largest funds industry in the world and the largest in Europe. In this article we look at the Pillar 2 impact on Luxembourg private debt funds.