A Review of China’s Tax Law From a Pillar Two Perspective

In this analysis we look at the key features of China’s tax law that would need to be taken into account by MNEs with Chinese subsidiaries for Pillar 2 purposes.

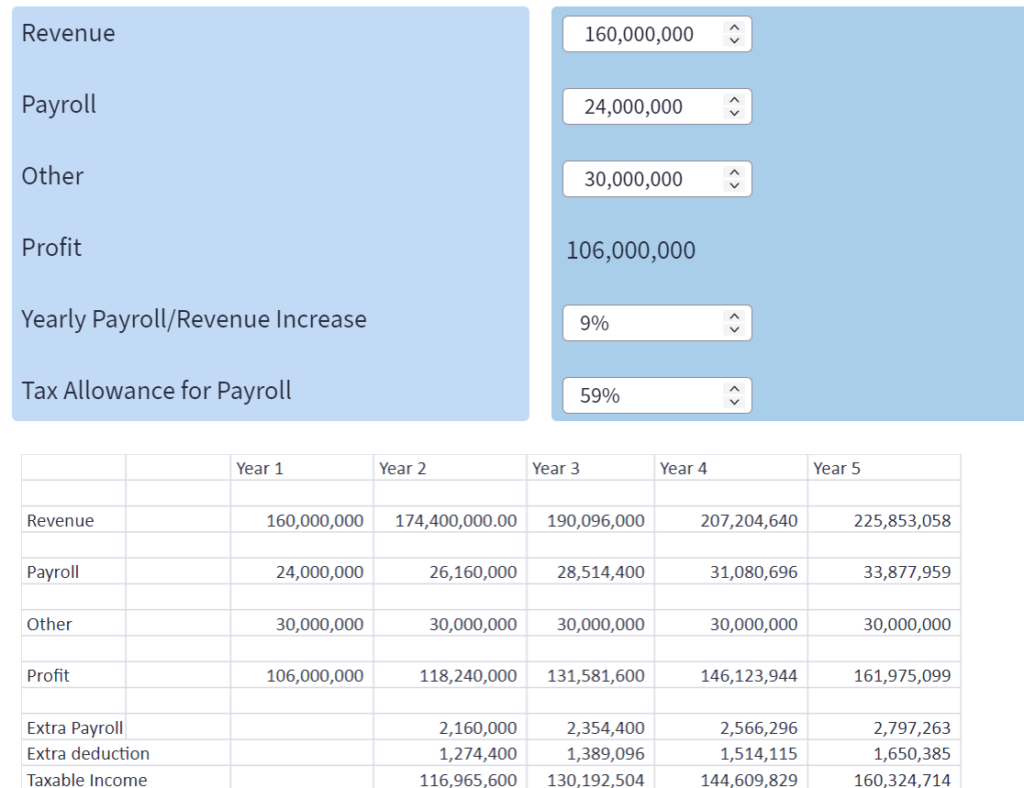

Payroll Tax Incentives – Pillar Two Modelling Tool

This Modelling Tool accompanies our analysis Modelling the Impact of Payroll Tax Incentives Post Pillar 2. Members use this tool to adjust key variables.

Modelling the Impact of Payroll Tax Incentives Post Pillar 2

In a post Pillar Two environment, the nature of tax incentives needs to be carefully considered to ensure that both MNEs and tax authorities derive benefits. In this analysis we model the impact of payroll tax incentives.

India’s Tax Regime after Pillar Two: Key Risks and Opportunities

In this article we look at India’s corporate income tax regime and assess the impact of the Pillar Two GloBE Rules on MNE’s with operations in India.

The Thorny Issue of Pillar Two in Vietnam

Vietnam’s broad income-based tax incentives could impact on investment into Vietnam in a post Pillar Two environment. We look at the issues and policy options.

Highlights of the OECD Progress Report on the Administration of Amount A

On October 6, 2022, the OECD issued the Progress Report on the Administration and Tax Certainty Aspects of Amount A of Pillar One (the ‘Progress Report’), which includes draft Model Rules on the administration of Amount A.

Global Developments with Pillars 1 & 2 Last Week

In this members article we look at key developments last week, including Ireland, Vietnam, Belgium and the OECD.

Malaysia to Implement Global Minimum Tax & QDMTT in 2024

In today’s 2023 Budget Speech, the Malaysian government joined the growing number of countries that will implement the 15% global minimum tax under Pillar 2.

Takeaways from Yesterday’s OECD Report on Tax Incentives & Pillar 2

The OECD issued a report yesterday on tax incentives after Pillar 2. We look at the key takeaways including which tax incentives have the largest impact.

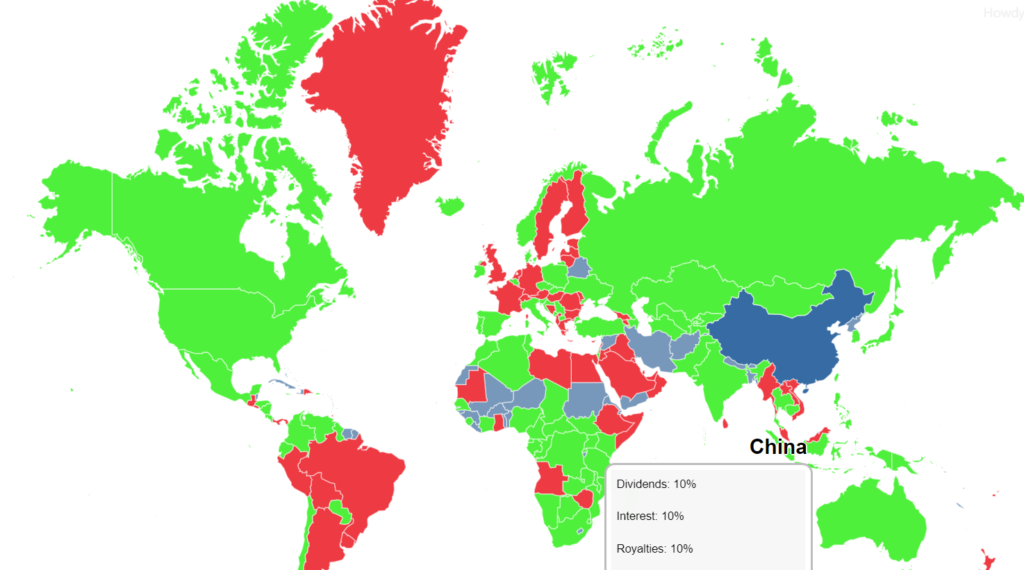

Subject-to-Tax Rule: Global Withholding Tax Map

The Subject-to-Tax Rule is a key component of Pillar Two, and unlike the GloBE Rules focuses on source jurisdictions. Our members-only global map highlights domestic withholding taxes at less than the 9% rate under the Subject-to-Tax Rule.