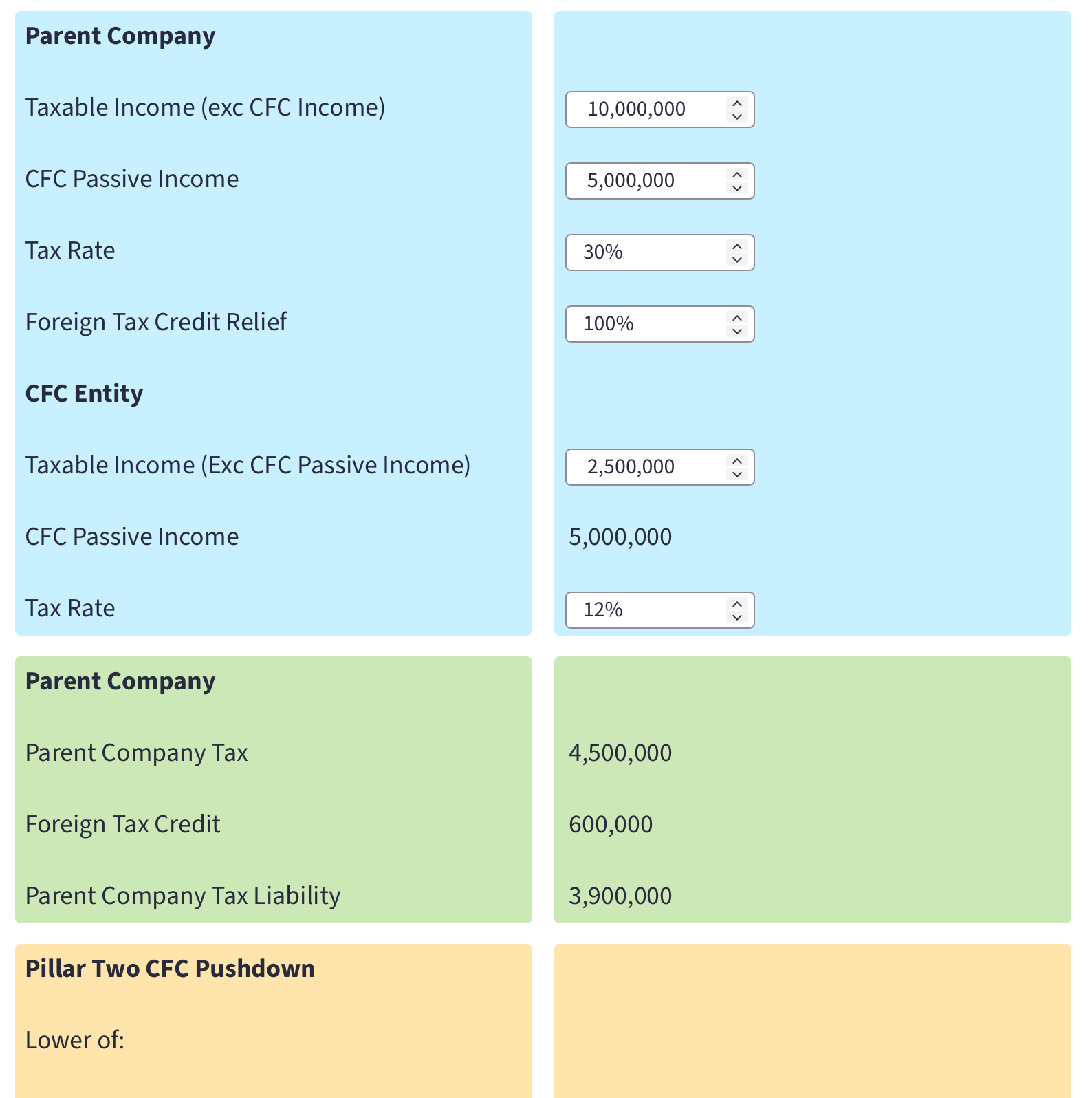

CFC Pushdown Limitation Tool

When allocating taxes to group entities for the purpose of the Pillar Two rules, tax paid by a parent entity under a controlled foreign company (CFC) regime is usually allocated to the CFC entity. However, under Pillar Two, this is subject to a limitation. Use our interactive tool to see the impact of the CFC pushdown limitation.