New: Pillar Two Workflow - generate GIR/GloBE, safe harbour and evidence workflows in one workspace.

Open Workflow Beta

Cloud-Based Software for Unrivalled Pillar Two Analytics and Insights

Our cloud-based Pillar Two software provides access to market-leading analysis and insights to allow you to model the impact of the Pillar Two GloBE Rules on any potential top-up tax liability, determine best and worst case scenarios and simulate the impact of making various Pillar Two elections.

Free DownloadA free downloadable version of the Pillar Two Tax Engine is available for members opting for the Annual Membership. To access, please Click Here.

Key Features

Cloud-based data input allows for a collaborative approach to data entry. Multiple teams can work on a single file to simplify the data entry requirements.

The backend data entry can be configured to pull data from various ERP systems.

Analysis and insights are provided by a front-end web portal in your private membership account.

The cloud input data syncs with the web portal in a split second, meaning your analysis and insights are always up to date.

Analytics and Insights

Calculate Pillar Two Top-Up Tax and Model the Impact on Your ETR

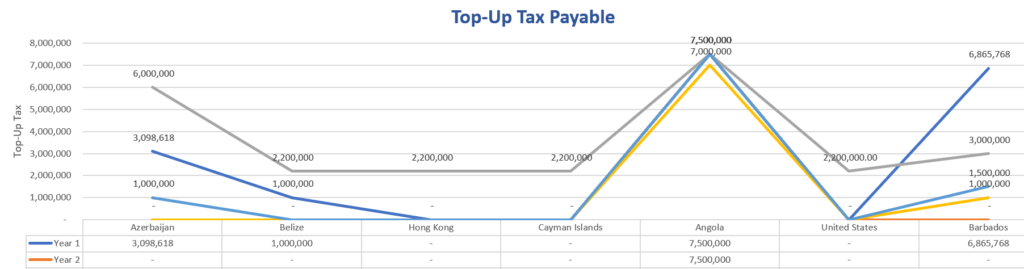

Determine potential Pillar Two jurisdictional top-up tax liabilities over a 5-year period

Identify the impact on your global and jurisdictional ETR

The software handles all the jurisdictional blending calculations as well as GloBE income and tax adjustments, including deferred tax

Interactive graphs and charts to instantly see key takeaways

Easily Adjust Assets and Payroll to See the Impact on your Top-Up Tax Liability

The Substance-Based Income Exclusion directly reduces Pillar Two GloBE income subject to top-up tax.

Model the impact of changes to jurisdictional tangible fixed assets and/or payroll on top-up tax liabilities via the substance-based income exclusion.

Model the Impact of Making a GloBE Loss Deferred Tax Asset Election

The GloBE Loss Deferred Tax Asset Election eliminates the deferred tax entries from the financial accounts (and any GloBE adjustments) when determining the Pillar Two top-up tax. Instead, a loss carry-forward is created which operates in a similar way to a deferred tax asset.

This is a key election, as it is a ‘once and for all’ election.

Use the Pillar Two Tax Engine to instantly assess whether it is advantageous to make a GloBE Loss Deferred Tax Asset Election.

Model the Impact of Making an Election to Spread Capital Gains

The Election to Spread Capital Gains allows capital gains to be carried back for 4-years and allocated amongst the jurisdictional entities.

Determine the impact of making an Election to Spread Capital Gains.

Model the Impact of Making an Stock-Based Compensation Election

The Stock-Based Compensation Election replaces the relevant entry in the financial accounts with the tax deduction.

Use the Pillar Two Tax Engine to instantly see the effect of making a Stock-Based Compensation Election on your top-up tax liability.

Detailed Supporting Workings

Supported by detailed workings to allow you to track the impact of changes and adjustments.

Living Software

New features are added on a weekly basis. Subscribers have access to all updates which will automatically be available via the cloud-based data entry system and in your membership portal.

We use cookies on our website to give you the most relevant experience. By clicking “Accept All”, you consent to the use of all the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.