Canada Issues Instructions for Filing Pillar 2 Returns

In January 2026, Canada issued the filing procedures for the GIR, GMT Return and the Double Filing Relief Notification.

Korea Issues Amendments to its Enforcement Decree for Pillar 2 Updates

On January 19, 2026, South Korea issued a Draft Law to amend the Enforcement Decree to the International Tax Adjustment Act. This provides for detailed provisions for the application of the QDMTT and will also extend the Transitional CbCR Safe Harbour by 1 year (as provided in the January 2026 OECD Side-by-Side Package).

Hong Kong Opens its Pillar 2 E-Filing Portal

On January 19, 2026, the Hong Kong Inland Revenue Department opened its E-filing portal for the submission of Top-Up Tax Notifications

Israel Enacts its DMTT Law with Significant Changes from the Previous Draft law

On December 31, 2025, Israel enacted Law No. Law 5776-2025 on the Minimum Corporate Tax for Multinational Groups. The enacted law contains some significant changes from the previous draft law.

Uruguay Enacts DMTT Law and issues a Decree for Exemptions under Tax Stability Agreements

On December 29, 2025, Uruguay’s President issued Decree No. 325/025, to provide for exemptions from the QDMTT for entities covered by a tax stability agreement. Note that Law N° 20446 to enact the QDMTT was published in the Official Gazette on January 8, 2026.

South Korea Enacts 2026 Tax Reform for QDMTT Implementation

On December 23, 2025, Korea enacted Law number 21215 to implement the 2026 Tax Reform. This includes a QDMTT from January 1, 2026.

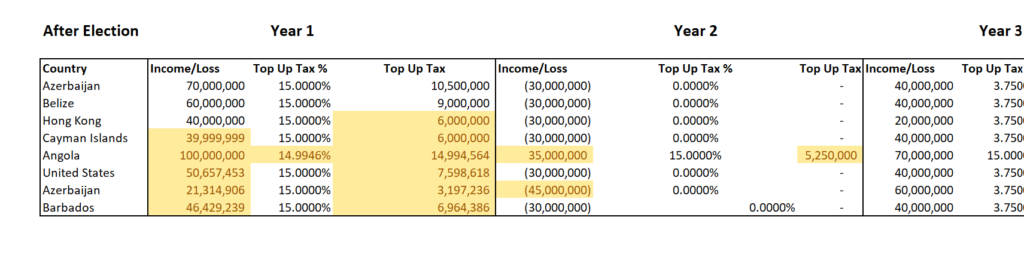

Sample Excel File for the Simplified ETR Safe Harbour

On January 5, 2026, the OECD Released Guidance on amendments to the Pillar 2 rules for the Side-by-Side Tax Package. This includes a new Simplified ETR Safe Harbour from December 31, 2026 (December 31, 2025 in certain cases). We provide an excel overview for the key elements of the Safe Harbour calculation.

Sample Calculator for the New Substance-based Tax Incentive Safe Harbour

On January 5, 2026, the OECD Released Guidance on amendments to the Pillar 2 rules for the Side-by-Side Tax Package. This includes a new Substance-based Tax Incentive Safe Harbour. This online tool shows how the new safe harbour operates.

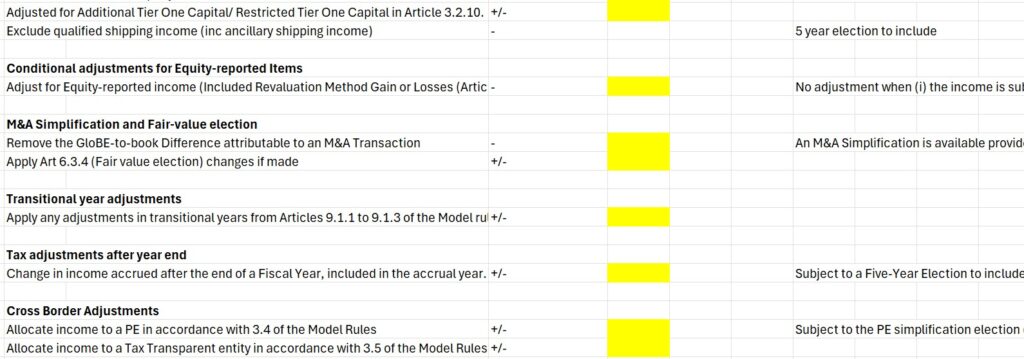

New Elections in the OECD Side-by-Side Package

On January 5, 2026, the OECD Released Guidance on amendments to the Pillar 2 rules for the Side-by-Side Tax Package. This article looks at a number of the new elections that arise from this.

OECD Releases Guidance on the Side-by-Side Package

On January 5, 2026, the OECD Released Guidance on amendments to the Pillar 2 rules for the Side-by-Side Tax Package.