Analysis of South Korea’s Draft Pillar Two Law

On July 22, 2022, South Korea released a draft law to implement the OECD’s Pillar Two GloBE Rules (the ‘draft law’) in legislative notice 2022-128. Read our analysis.

Analysis of Switzerlands Draft Pillar Two Decree

On August 17, 2022, the Swiss Federal Council issued a draft decree for the implementation of Pillar Two of the OECDs Two Pillar Solution from January 1, 2024. Read our detailed analysis.

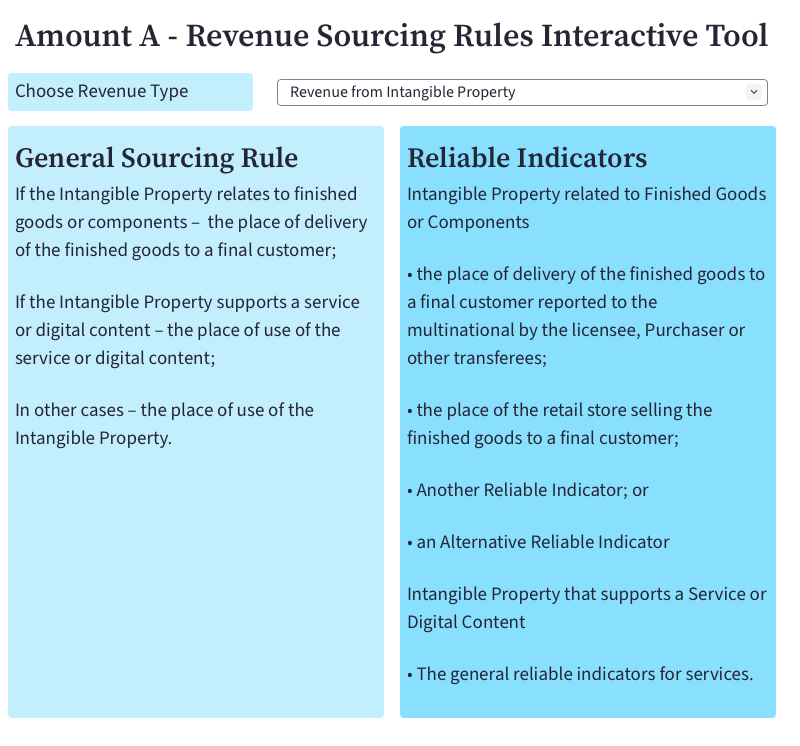

Pillar One: Amount A Revenue Sourcing Rules Interactive Tool

The Revenue Sourcing Rules for Amount A are used to determine where an in-scope multinational group derives its revenues. This is then used in the profit reallocation calculation.

Use our interactive tool to quickly determine the relevant sourcing rule for each revenue type.

Pillar One Reliable Indicators – An Analysis

The Amount A reliable indicators are the practical methods of allocating revenue to jurisdictions for the purposes of the Pillar One, Amount A revenue sourcing rules.

Allocation Keys for Sourcing Revenue under Amount A

Allocation Keys are a key aspect of the Amount A Revenue Sourcing Rules, which attribute revenue to the jurisdictions an MNE group operates in. This is then used when determining how much profit is reallocated to a jurisdiction.

Marketing and Distribution Profits Safe Harbour: An Example

The marketing and distribution profits safe harbour is included in Articles 6(3)-(6) of the Progress Report on Amount A of Pillar One. It is deducted from the initial amount of profits reallocated to a jurisdiction (but cannot reduce profits below zero). One of the purposes of the safe harbour is to prevent double taxation, where […]

GloBE Loss Election – Interactive Tool

Our GloBE Loss Election interactive tool allows you simulate the impact on your top-up tax liability depending on whether a GloBE Loss Election is made or not.

Malaysia Confirms It Intends To Implement Pillar Two

The Chief Executive of Malaysia’s Inland Revenue Board has confirmed that Malaysia intends to push ahead with the implementation of Pillar Two.

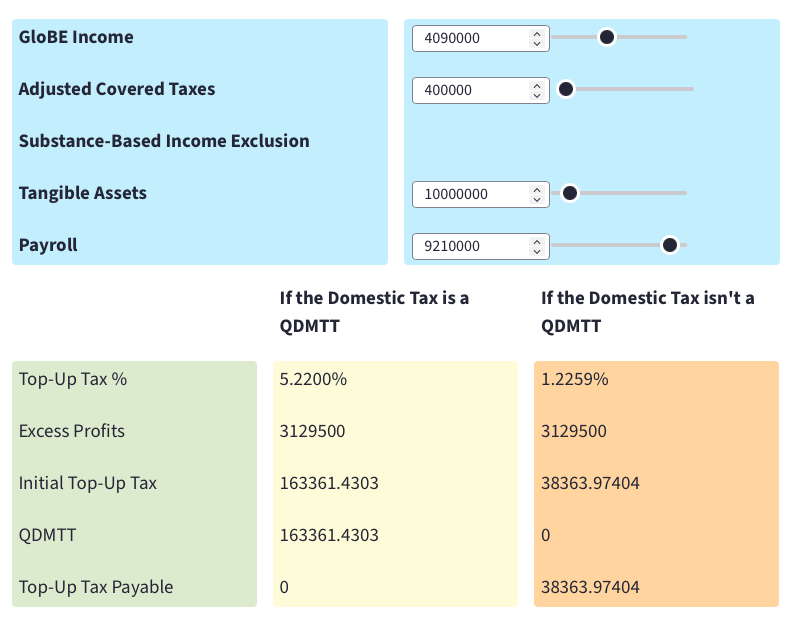

Pillar Two: Domestic Minimum Tax – Interactive Tool

Our Qualified Domestic Minimum Top-Up Tax (QDMTT) interactive tool allows you simulate the impact on your top-up tax liability depending on whether the domestic top-up tax is a QDMTT or is non-qualifying.

Mauritius 2022 Finance Bill includes Pillar Two Top-Up Tax

Mauritius 2022 Finance Act includes Pillar Two Top-Up Tax The Finance (Miscellaneous Provisions) Bill 2022 (subsequently enacted with very minor amendments in the Finance (Miscellaneous Provisions) Act 2022 on August 2, 2022) which implements provisions of the 2022 Budget in Mauritius includes mention of a qualified domestic minimum top-up tax for Pillar Two purposes. It’s a […]