Members Flowchart for the Deferred Tax Adjustment Amount

The Total Deferred Tax Adjustment Amount is a key element of the Pillar Two effective tax rate calculation. See our members flowchart which guides you though the calculation.

Pillar Two GloBE Loss Election – Friend or Foe?

The Pillar Two GloBE loss election can only be made once per jurisdiction. Therefore it’s essential to identity whether this will be beneficial or not. There may be some cases (such as where there is no deferred tax in a jurisdiction or where corporate income tax rates are very low) that this could swing the balance in favour of making an election. But what about the impact of other timing differences? In this article we look at the pro’s and con’s of making a GloBE loss election, including examples to illustrate key issues.

What MNE Groups need to be doing from December 1, 2021

The Pillar Two rules include a number of transitional rules that apply to MNEs from December 1, 2021. In this members article we look at the adjustments and tracking impact for MNE groups.

UK Multinational Top-Up Tax Calculator

The UK published draft legislation on July 20, 2022, to implement a ‘multinational top-up tax’ in line with Pillar Two of the OECDs Two-Pillar Solution. We have produced a calculator to illustrate the key aspects to the calculation of the multinational top-up tax.

A Review of the UK Draft Pillar Two Legislation

The UK published draft legislation on July 20, 2022 to implement Pillar Two from December 31, 2023. Whilst similar to the OECD Model Rules there are differences, not least the treatment of capital gain carry-backs.

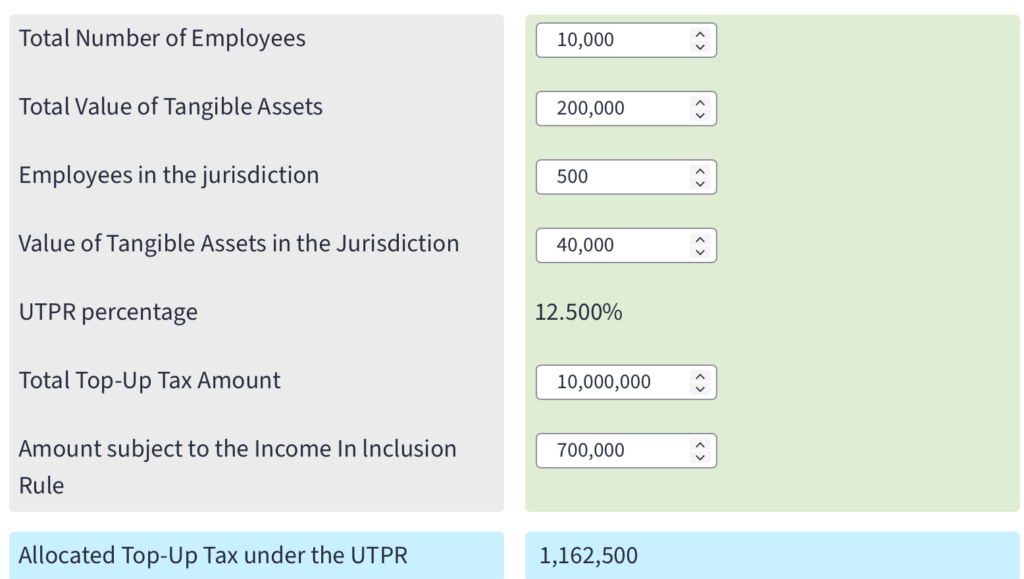

UTPR Calculator

This Pillar Two under-taxed payments rule (UTPR) calculator gives an indication of the broad operation of how the top-up tax is allocated to UTPR jurisdictions.

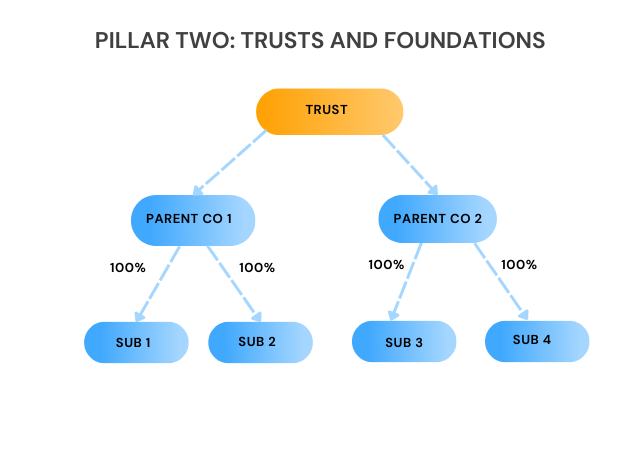

How does Pillar Two Impact Trusts and Foundations?

The Pillar Two rules don’t just apply to companies. They apply to ‘entities’ which can include Trusts and Foundations. The application of the Pillar Two rules to Trusts and Foundations can give rise to a number of issues. Read our member article on some of the practical issues to consider.

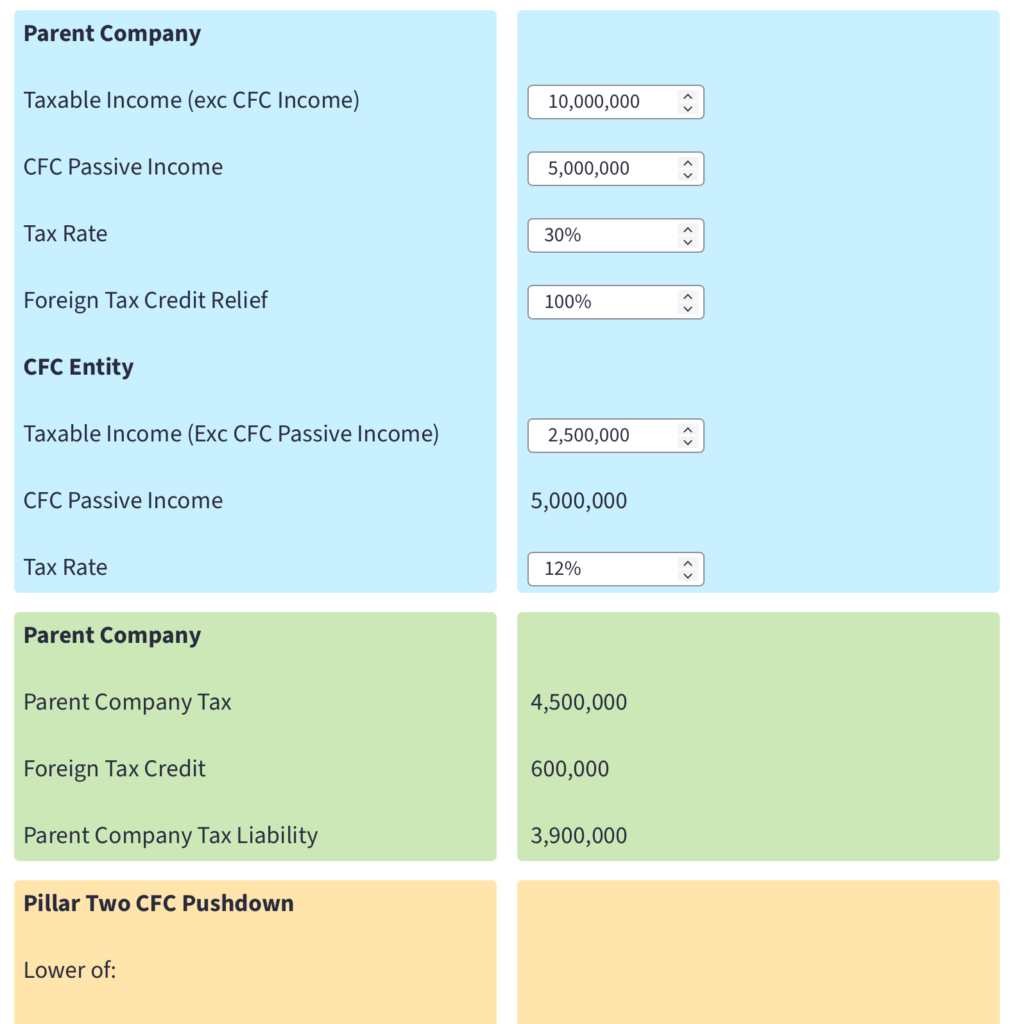

CFC Pushdown Limitation Tool

When allocating taxes to group entities for the purpose of the Pillar Two rules, tax paid by a parent entity under a controlled foreign company (CFC) regime is usually allocated to the CFC entity. However, under Pillar Two, this is subject to a limitation. Use our interactive tool to see the impact of the CFC pushdown limitation.

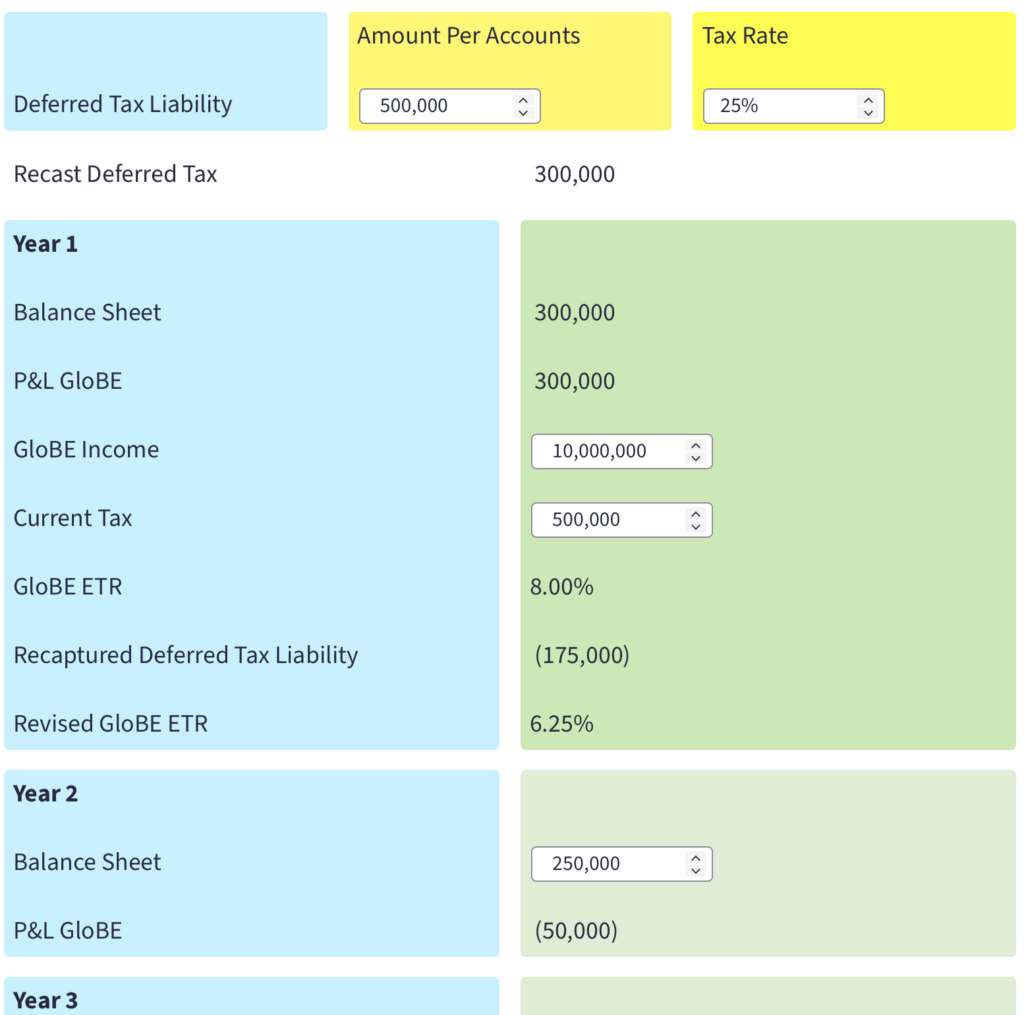

Pillar Two Deferred Tax Recapture Tool

Our deferred tax recapture tool simulates the impact of the Pillar Two rule that recaptures deferred tax liabilities that are not paid within five years.

Pillar Two Deferred Tax Liability Calculator

Deferred Tax has a significant impact on the Pillar Two effective tax rate (ETR) and therefore on any top-up tax that may be levied. Use our Pillar Two Deferred Tax Liability Calculator to model the impact on the Pillar Two top-up tax.