How does Pillar One Tie into Pillar Two?

Although Pillar One and Pillar Two are largely separate, the draft Pillar One rules issued by the OECD on July 11, 2022 include some interesting overlaps with Pillar Two. Read our analysis of how Pillar One ties into Pillar Two.

Pillar One Profit Allocation Calculator

On July 11, 2022, the OECD released a progress report on its Two Pillar Solution. This included draft rules on Pillar One. Whilst these draft rules are subject to a consultation, they nevertheless make interesting reading, particularly as there has, to date, been very little detailed information on the marketing and distribution profits safe harbour. Use our Pillar One profit allocation calculator to see the impact of the profit reallocation and marketing and distribution profits safe harbour.

Pillar Two Implementation is Inescapable

This is according to an OECD progress report issued yesterday which states that “…implementation of the global minimum corporate tax seems ineluctable.” Whilst mainly focusing on Pillar One of the Two-Pillar framework, the report does provide a useful update on the status of Pillar Two’s global implementation and the OECDs opinion on how its progressing.

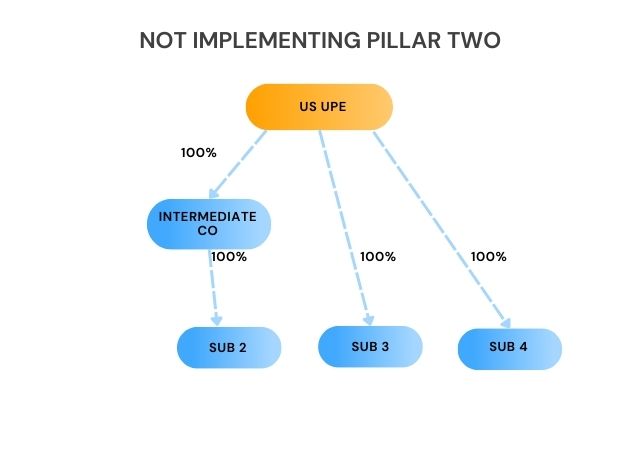

What Happens if the US Doesn’t Implement Pillar Two?

There’s been a lot of speculation as to whether the US in particular will be able to enact legislation to implement Pillar Two in the near future. This then raises the question as to exactly what would happen?

The answer depends on whether the ‘tipping point’ has been reached. The Pillar Two rules depend on a certain critical mass of jurisdictions implementing Pillar Two. Once this point is reached there would be significant disadvantages to not implementing Pillar Two.

Use our Capital Gains Carry Back Tool

Our capital gains carry back tool models the impact of making a Pillar Two election to spread capital gains. View different scenarios by changing gains and losses.

Why most MNEs won’t benefit from the substance-based exclusion

The substance-based income exclusion is one of the key carve-outs in the GloBE income calculation. It provides a measure of relief from the Pillar Two top-up tax for an MNEs payroll and tangible fixed asset costs in a jurisdiction. The idea behind this is that the Pillar Two rules are aimed in part at combatting […]

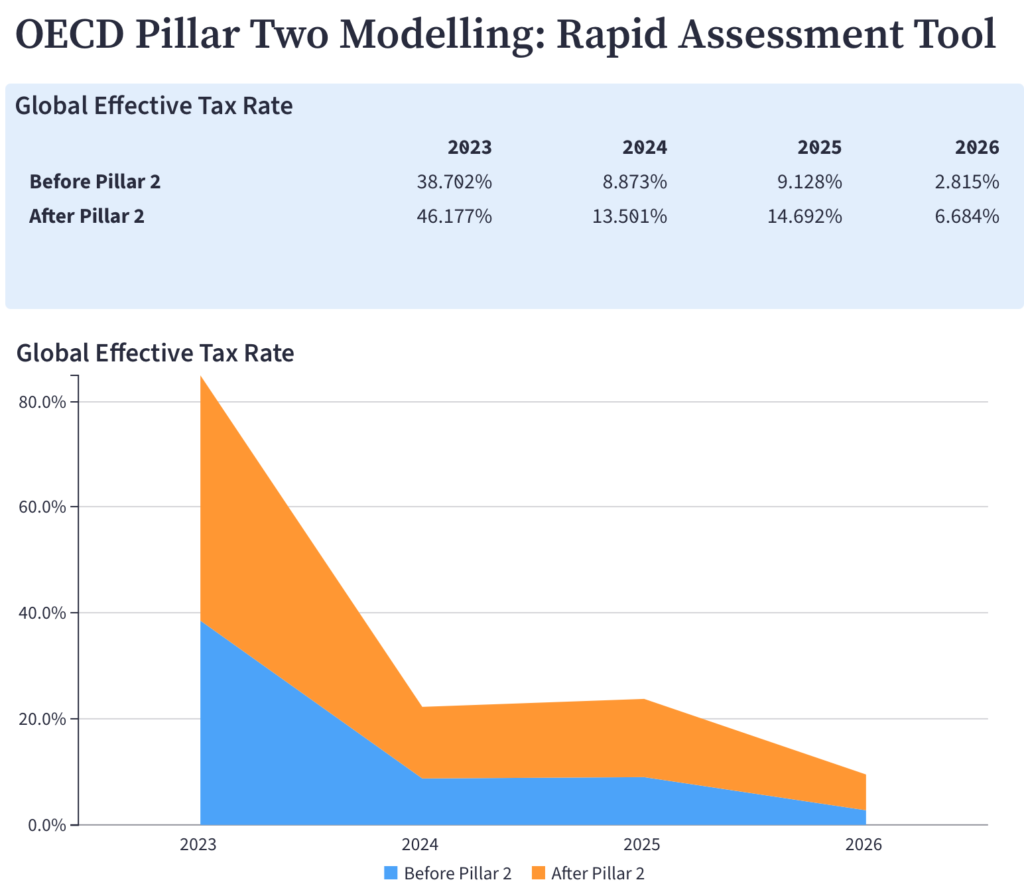

Rapid Assessment Tool

Our Pillar Two Rapid Assessment Tool, simulates the impact of the Pillar Two GloBE Rules. It is a slimmed-down version of our Pillar Two Tax Engine. This version handles 4 companies and calculates all of the jurisdictional blending and top-up tax calculations. Simply input jurisdictions, company details and enter as much financial information as you […]

Jerseys Approach to the Implementation of Pillar Two

The Jersey government issued a tax policy paper on the implementation of Pillar Two. In this members-only article, we look at the options discussed and the impact on MNE groups with holding companies and subsidiaries in Jersey.

Pillar Two Deferred Tax Asset Calculator

Deferred Tax is a key element of the Pillar Two Rules, aimed at smoothing out the effective tax rate to address timing differences. This simple Pillar Two deferred tax calculator shows the broad operation of a deferred tax asset and its impact on the effective tax rate and top-up tax.

An Analysis of Tax Incentives in Latin America and the impact of Pillar Two

Latin American countries tend to have relatively high nominal corporate income tax rates, but they can offer significant tax incentives that can push the effective tax rate down substantially.