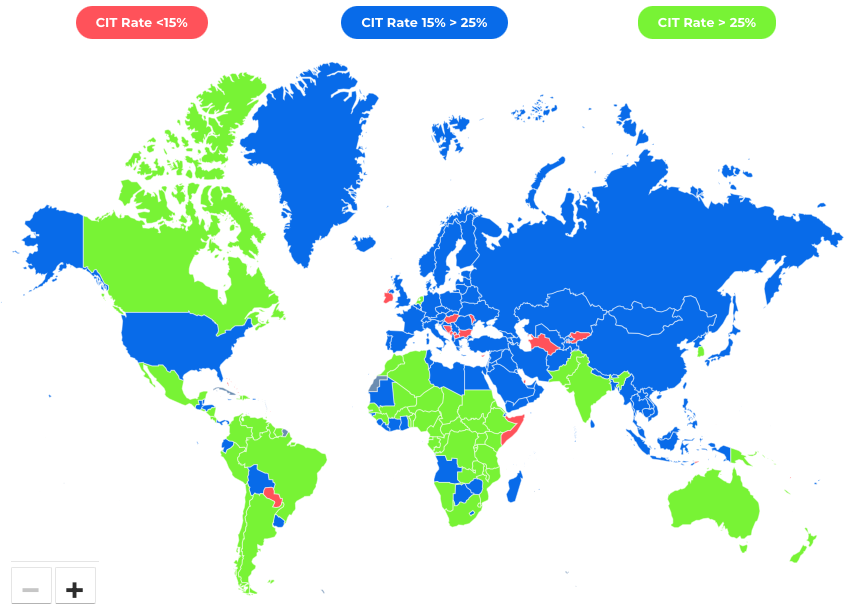

Interactive Map: Countries with 2022 CIT Rates Below 15%

Our interactive map breaks down worldwide corporate income tax rates to identify jurisdictions with a headline CIT rate below the Pillar Two 15% rate.

Our interactive map breaks down worldwide corporate income tax rates to identify jurisdictions with a headline CIT rate below the Pillar Two 15% rate.

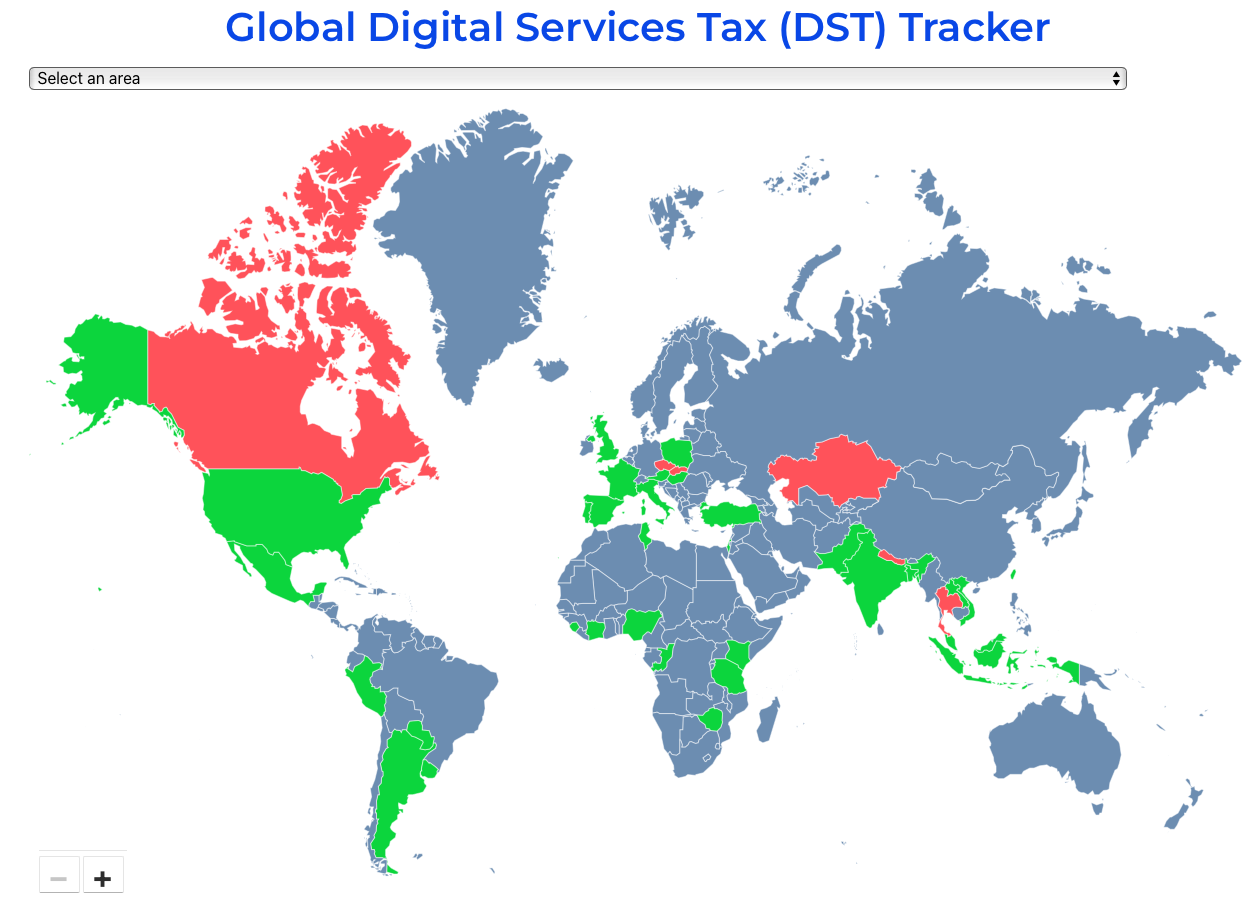

Our Global Digital Services Tax Tracker allows you to stay up to date with international digital service taxes. Cited and with links to domestic legislation.

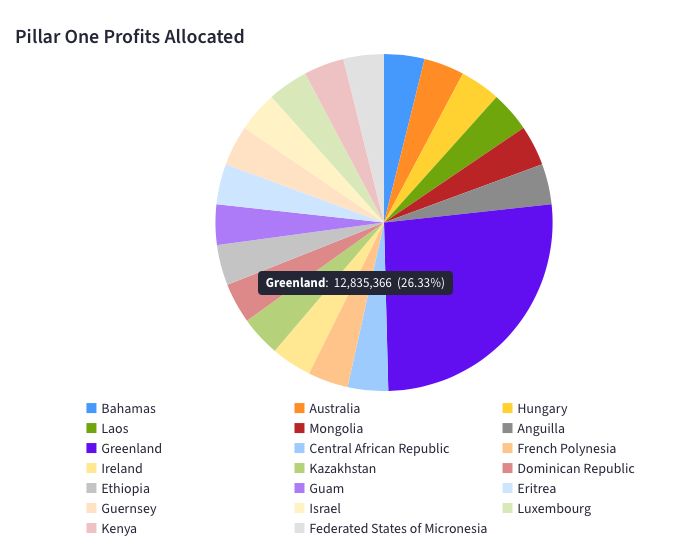

Our OECD Pillar One Modelling Tool is designed to provide an analysis of the high-level impact of Amount A of Pillar One.

Our OECD Pillar One & Two Modelling Tool is designed to provide an analysis of the high-level impact of Amount A of Pillar One. Key

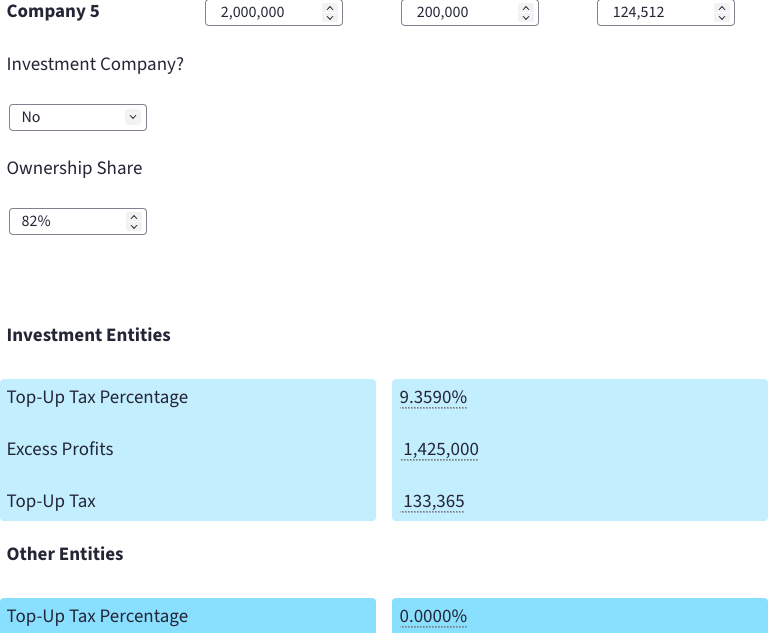

Our Investment Companies Top-Up Tax Calculator models the impact of Pillar Two in a jurisdiction where there are a mix of investment and non-investment companies.

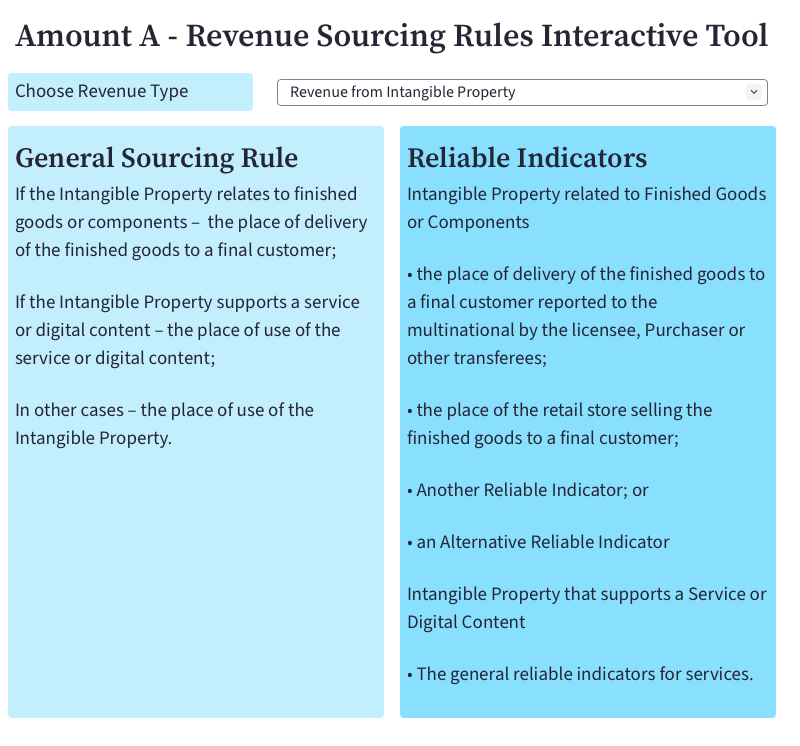

The Revenue Sourcing Rules for Amount A are used to determine where an in-scope multinational group derives its revenues. This is then used in the profit reallocation calculation.

Use our interactive tool to quickly determine the relevant sourcing rule for each revenue type.

Our GloBE Loss Election interactive tool allows you simulate the impact on your top-up tax liability depending on whether a GloBE Loss Election is made or not.

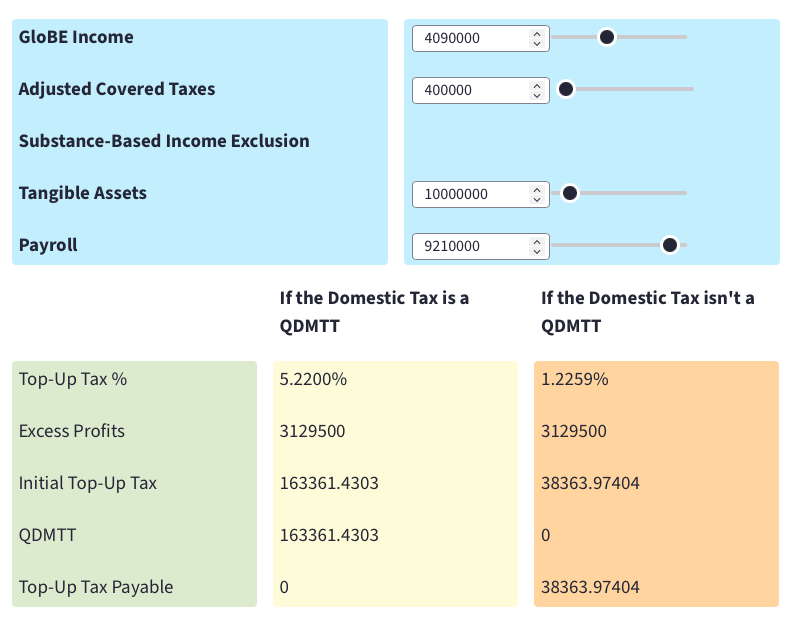

Our Qualified Domestic Minimum Top-Up Tax (QDMTT) interactive tool allows you simulate the impact on your top-up tax liability depending on whether the domestic top-up tax is a QDMTT or is non-qualifying.

The UK published draft legislation on July 20, 2022, to implement a ‘multinational top-up tax’ in line with Pillar Two of the OECDs Two-Pillar Solution. We have produced a calculator to illustrate the key aspects to the calculation of the multinational top-up tax.

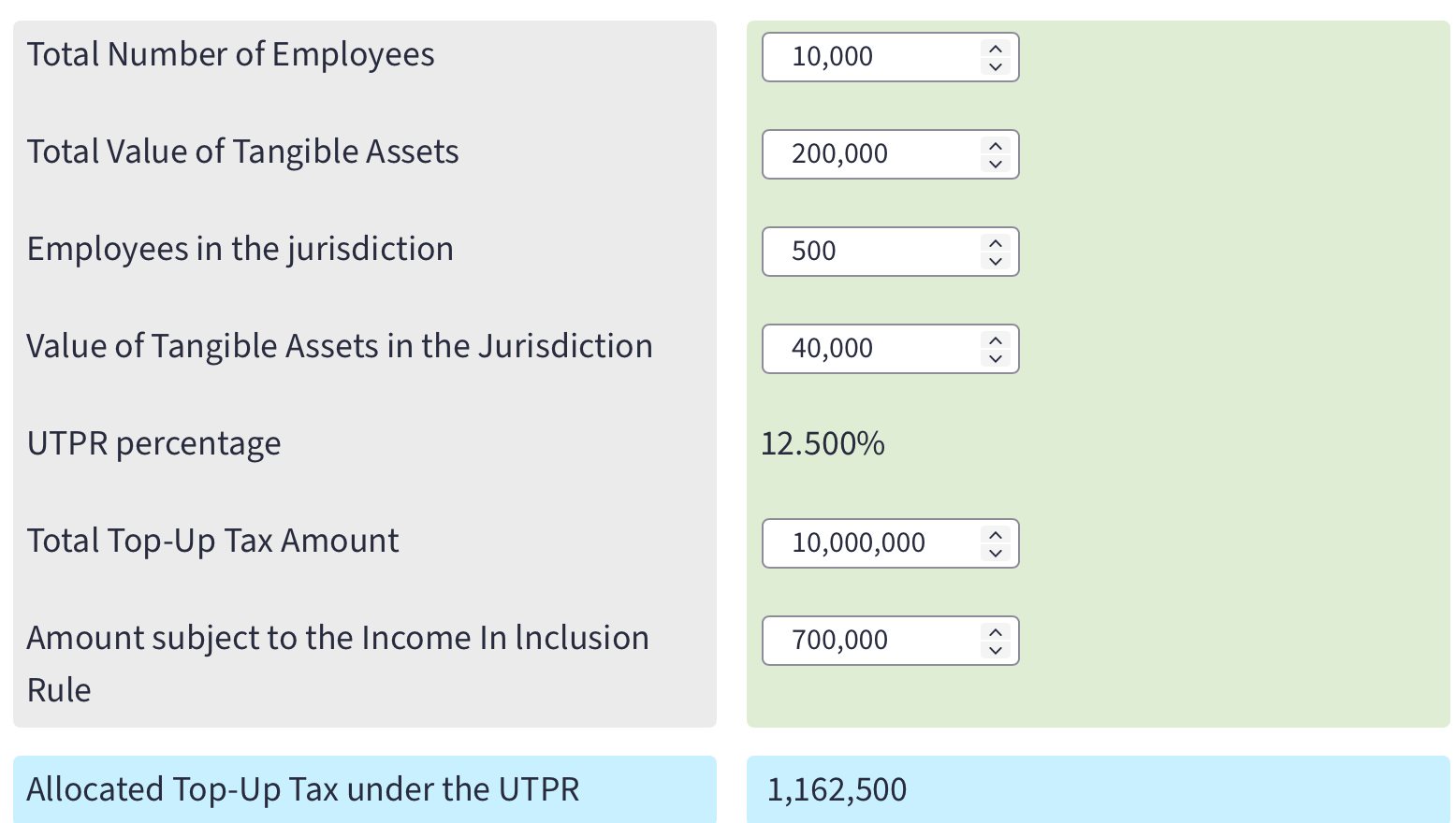

This Pillar Two under-taxed payments rule (UTPR) calculator gives an indication of the broad operation of how the top-up tax is allocated to UTPR jurisdictions.