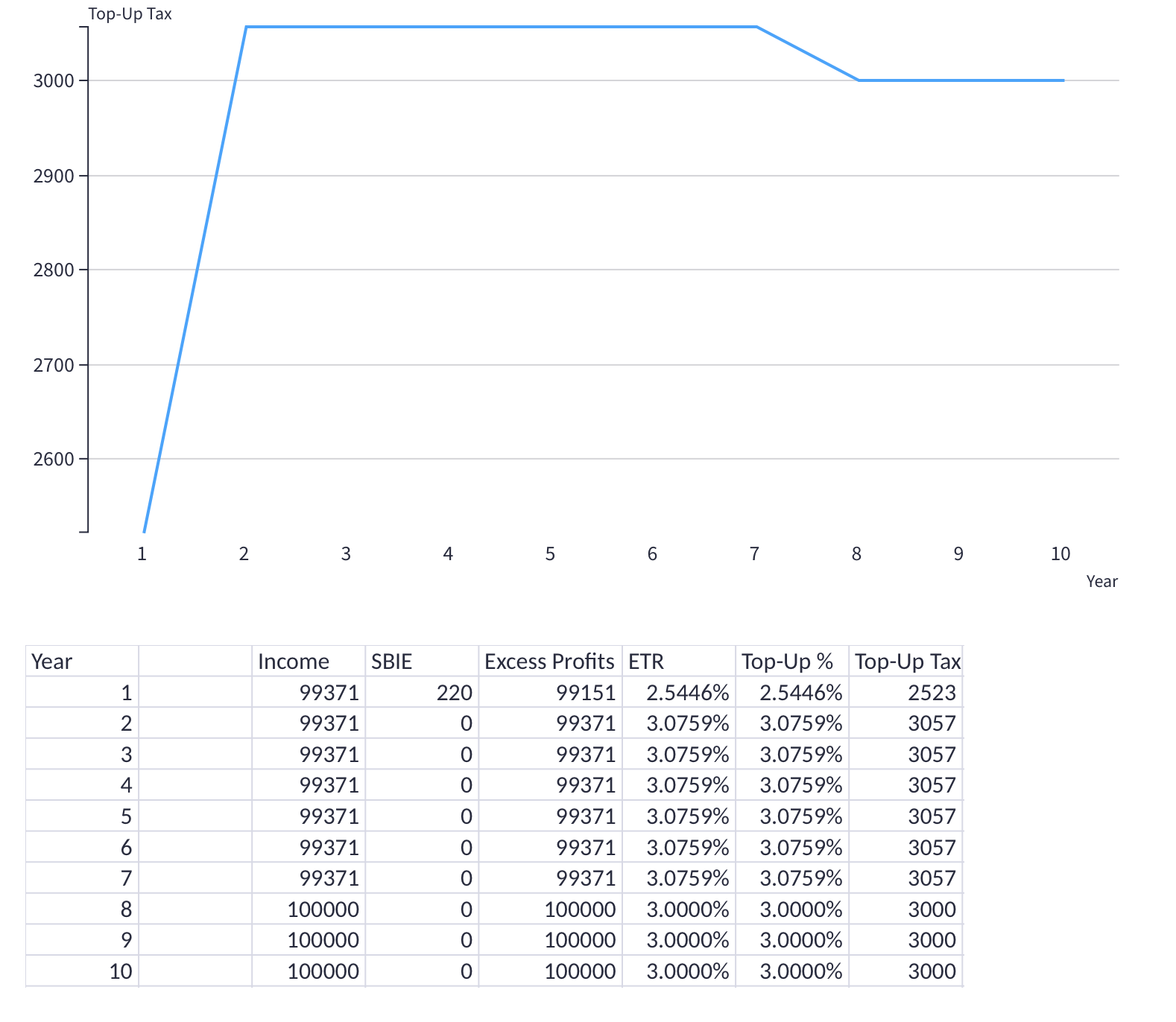

Accelerated Capital Allowances & SBIE Tool

For Pillar Two purposes, investments in fixed assets can involve an interaction between deferred tax impacts and the the substance-based income exclusion.

For Pillar Two purposes, investments in fixed assets can involve an interaction between deferred tax impacts and the the substance-based income exclusion.

IAS 1, IAS 10 and IAS 12 all have provisions that can impact on the required disclosures in financial statements for Pillar Two, however, the key determinant will be whether the domestic tax law to implement the Pillar Two GloBE Rules has been announced, substantively enacted, or enacted before the financial statements are issued.

Identifying the data points required to apply the Pillar 2 rules is the first step in any tax data mapping MNEs undertake. We list the key 122 data points.

Whilst Pillar 1 and Pillar 2 are separate and independent of each other, there are areas where they overlap, most notably the inclusion of Pillar 1 tax for Pillar 2 purposes and the overlap in some of the adjusted profits definitions.

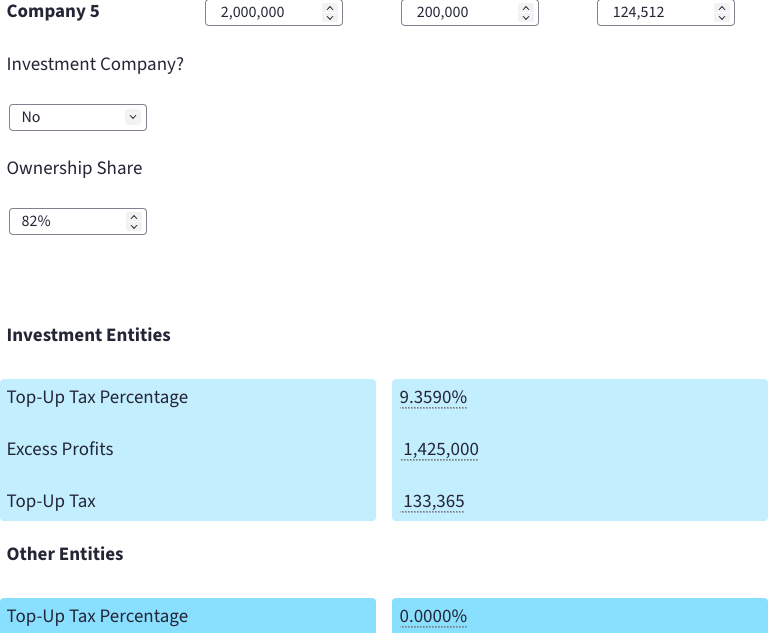

Our Investment Companies Top-Up Tax Calculator models the impact of Pillar Two in a jurisdiction where there are a mix of investment and non-investment companies.

Our GloBE Loss Election interactive tool allows you simulate the impact on your top-up tax liability depending on whether a GloBE Loss Election is made or not.

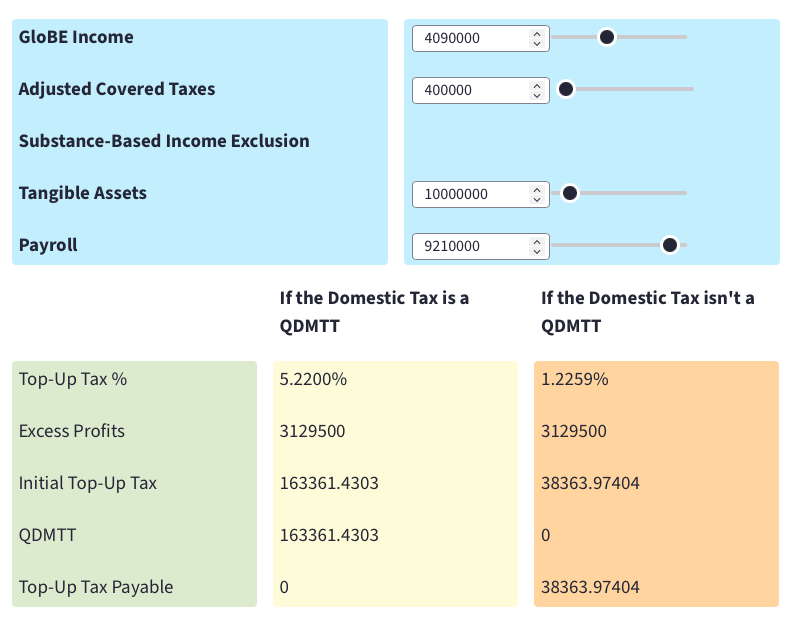

Our Qualified Domestic Minimum Top-Up Tax (QDMTT) interactive tool allows you simulate the impact on your top-up tax liability depending on whether the domestic top-up tax is a QDMTT or is non-qualifying.

The Pillar Two rules include a number of transitional rules that apply to MNEs from December 1, 2021. In this members article we look at the adjustments and tracking impact for MNE groups.

The UK published draft legislation on July 20, 2022, to implement a ‘multinational top-up tax’ in line with Pillar Two of the OECDs Two-Pillar Solution. We have produced a calculator to illustrate the key aspects to the calculation of the multinational top-up tax.

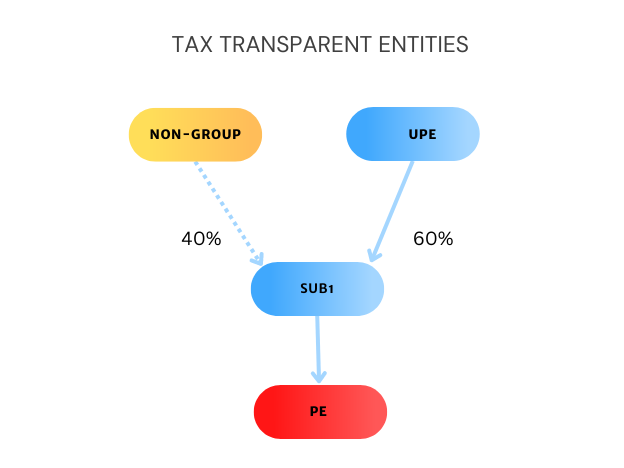

Permanent Establishments (PEs) are subject to a number of specific rules under Pillar Two in order to apply the general provisions to them. Key issues are what is a PE under Pillar Two? where is it located? and how are income and taxes allocated to it?