Germany Pillar Two Filing Guide

A practical guide to Germany’s Registration, group head notification and GloBE Information Return (GIR) filing through the BZSt framework

A practical guide to Germany’s Registration, group head notification and GloBE Information Return (GIR) filing through the BZSt framework

Australia issued the Taxation (Multinational—Global and Domestic Minimum Tax) (Qualified GloBE Taxes) Amendment (Measures No. 1) Determination 2026, on March 20, 2026. This updates Australia’s domestic lists of foreign Qualified IIRs, foreign Qualified Domestic Minimum Top-up Taxes, and jurisdictions with QDMTT Safe Harbour status

On March 24, 2026, Finland gazetted a law amending its Minimum Tax Act to provide for aspects of the January 2026 OECD Side By Side Tax Package and the June 2024 and January 2025 OECD Administrative Guidance.

On March 24, 2026, Belgium issued an updated draft QDMTT Form and XSD Schema.

A practical guide to Luxembourg’s top-up tax return on MyGuichet.lu, including what the local XML does, which fields drive the filing logic, and where groups usually need extra controls.

On February 27, 2026, South Korea issued an amendment to its international tax adjustment decree to provide for detailed provisions for the application of its QDMTT.

In this article we look at how Japan handles the Pillar Two GloBE Information Return through the e-Tax Multinational Enterprise Information Reporting Corner, what fields Japan localises in the GIR XML and CSV package, and how that sits alongside the Japanese top-up tax return.

View our downloadable checklist for Japan’s Pillar Two filing process.

On March 17, 2026, Belgium issued a Circular on Pillar Two Currency Conversion.

On March 19, 2026, Belgium issued a Consultation on the Pillar 2 IIR Top-Up Tax Return.

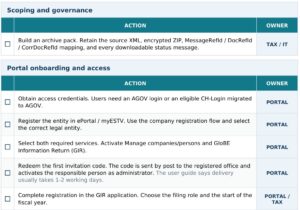

On March 19, 2026, Switzerland opened up its GIR Filing Portal. Download our Swiss GIR Filing Checklist.

On March 19, 2026, Switzerland opened up its GIR Filing Portal.