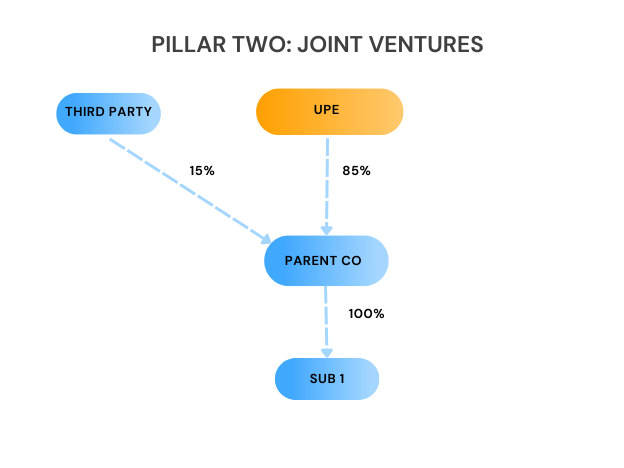

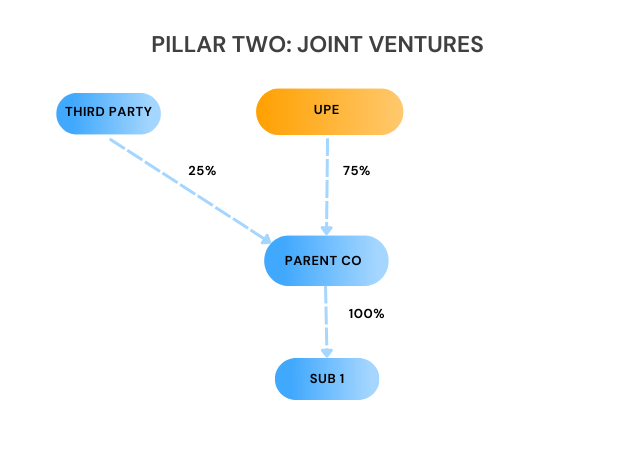

Joint Ventures (JVs) that aren’t consolidated are treated as follows:

1. The JV and any of its subsidiaries are treated as a separate MNE group for Pillar Two purposes, and the JV is treated as the UPE, under Article 6.4.1(a) of the OECD Model Rules.

This means that for the purposes of jurisdictional blending the JV group income and covered tax is not included with other entities in the jurisdiction.

2. The JV itself does not apply the income inclusion rule or the under-taxed payments rule, under Article 6.4.1(b) of the OECD Model Rules.

The standard rules apply and the UPE or other parent entity would apply an IIR.

3. The UPE or parent entity is subject to top-up tax on its allocable share of the JV group under Article 6.4.1(c) of the OECD Model Rules.

This takes into account both direct and indirect holdings.