Instead of applying the deferred tax rules (or for instance in jurisdictions where there is a very low rate of corporate income tax), an entity can make a Pillar Two GloBE loss election. For more information on deferred tax under Pillar Two, see Deferred Tax.

The GloBE Loss Election dispenses with the deferred tax expense and allows the MNE to establish a deemed deferred tax asset where this is a net Pillar Two GloBE loss for that jurisdiction. The deferred tax asset for the loss is equal to the net Pillar Two loss in the jurisdiction for a fiscal year, multiplied by the 15% minimum rate.

It is a jurisdictional election and is made in the first Pillar Two information return for the jurisdiction (ie it is a ‘once and for all’ election). For more information on the GloBE Loss Election, see GloBE Loss Election.

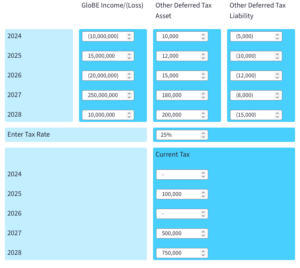

Members can use our interactive tool to see how the GloBE Loss Election operates and how it effects the Pillar Two top-up tax liability.

Enter details of income, losses, current tax and other deferred tax attributes and the tool calculates the estimated top-up tax with and without making a GloBE Loss Election.

This website is not affiliated with or related to the OECD. We provide independent insights and analysis on the OECD Two-Pillar Solution

© 2026 OECDPillars.com

All Rights Reserved

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |