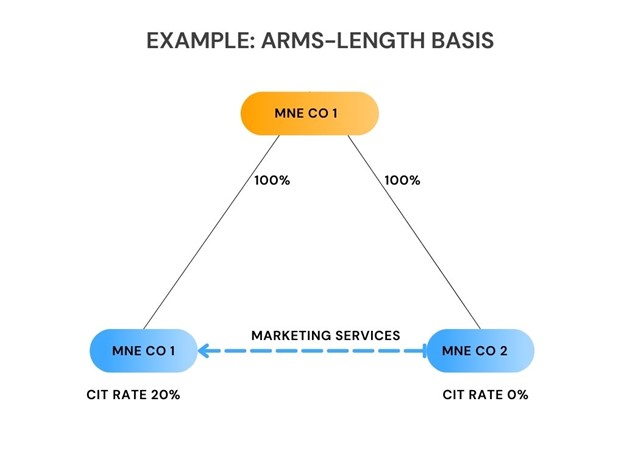

MNECo2 provided group marketing services to MNECo1. The financial accounts of both MNECo1 and MNECo2 reflect expenses and income of 5,000,000 euros.

However, for tax purposes, MNECo1 deducts 7,500,000 euros.

In this case, 2,500,000 euros is effectively not subject to tax in Country A and is not subject to top-up tax in Country B.

As such, to apply the arms-length requirement MNECo1 is required to add back 2,500,000 euros of its expense for the Pillar Two GloBE income calculation, and MNECo2 is required to reflect additional income of 2,500,000 euros in its Pillar Two GloBE income calculation.

Adjustments can also apply when there is a unilateral transfer pricing adjustment.

For instance, if in the above example MNECo1 had deducted an expense of 3,000,000 euros for tax purposes as a result of a unilateral transfer pricing adjustment, this would increase taxable income subject to corporate income tax by 2,000,000 euros in MNECo1, but that 2,000,000 of income is also subject to top-up tax in MNECo2.

Therefore, MNECo1 is required to reduce its expense in the calculation of Pillar Two GloBE income by 2,000,000 euros and MNECo2 is required to reduce its Pillar Two GloBE income by 2,000,000 euros.

Note that if the result of an adjustment to the arms-length basis would result in double taxation or non-taxation, then no adjustment is made.

For instance, if in the example above MNEco2 reflected income of 4,000,000 euros for tax purposes and the corporate income tax rate was 10%, no adjustment would be required.

Although the deduction in MNECo1 is 5,000,000 euros, this is included in Pillar Two GloBE income and is subject to top-up tax in MNECo2. Therefore, no adjustment is permitted.