Permanent Establishments (PEs)

As Permanent Establishments are treated as separate constituent entities for the purpose of the Pillar Two GloBE rules, there needs to be some way of allocating adjusted covered taxes to the PE for the purpose of calculating the jurisdictional ETR. For more information on PEs, see Pillar Two and Permanent Establishments.

In some cases, the main entity may not have separate financial statements for the PE, and the taxes paid by the PE may be included in the taxes incurred by the main entity.

Covered taxes are allocated to a PE under Article 4.3.2 of the OECD Model Rules by the following mechanism:

1. Identify the PE’s share of the main entity’s domestic taxable income. This should be able to be identified from the corporate income tax return process.

2. Identify the main entity’s tax liability arising from the PE’s taxable income. This is straightforward if the PE is subject to a separate tax rate. In other cases, the main entity’s tax liability (before any foreign tax credit) needs to be allocated to the PE.

3. Determine the amount of any tax credit allowed in the main entity in respect of the PE’s taxable income.

The tax determined using these steps is deducted from the covered tax for the main entity and allocated to the PE.

Special Rule for PE Losses

If there is a loss under the Pillar Two GloBE rules for a PE, Article 3.4.5 of the OECD Model Rules provides that this will be treated as an expense of the main entity to the extent that the loss of the PE is treated as an expense for domestic tax purposes.

Pillar Two GloBE income that is subsequently earned by the PE is treated as income of the main entity up to the amount treated as an expense by the main entity.

As the loss is allocated to the main entity, Article 4.3.4 of the OECD Model Rules provides that any adjusted covered taxes associated with the income are also allocated to the main entity up to the maximum corporate income tax on the income in the jurisdiction.

Note in this case, any deferred tax asset created and subsequently unwound in the main entity isn’t taken into account in adjusted covered taxes by either the PE or the main entity. This does not affect the treatment of the domestic law tax loss, which is subject to the general deferred tax regime.

Tax Transparent Entities

In the case of a tax transparent entity, the tax of the partner or member as determined above is allocated to the PE under Article 4.3.2(b) of the OECD Model Rules.

Any covered taxes that aren’t allocated to a PE are allocated to the entity owners (eg partners or members). If there is a reverse hybrid entity, just as for the allocation of Pillar Two GloBE income, covered taxes remain with the entity (aside from any amounts attributable to a PE).

Controlled Foreign Companies (CFCs)

The same approach taken to allocating covered tax to PEs can also be used to allocate covered taxes to CFCs under Article 4.3.2(c) of the OECD Model Rules, given this is essentially a similar scenario. Note, however, the below push-down limitation rule for passive income.

Hybrid Entities

A hybrid entity is an entity that is treated as opaque for tax purposes where it is located but tax transparent in the jurisdiction of its owners.

If the owner of a hybrid entity is a constituent entity that suffers tax on its share of the income of the hybrid entity (including withholding taxes), the covered taxes are allocated to the hybrid entity under Article 4.3.2(d) of the OECD Model Rules. The same three-step approach used to allocate covered taxes to a PE can also be used to calculate the covered taxes allocated to the hybrid entity.

Note, however, the below push-down limitation rule for passive income.

Tax on Dividends and Distributions

Withholding tax and other taxes (including net basis taxes) incurred on dividends received from another constituent entity are allocated to the distributing company under Article 4.3.2(e) of the OECD Model Rules.

This is notwithstanding the fact that the financial accounts of the receiving company will have accounted for any withholding tax in its current tax expense. Therefore, there would be a reduction in covered taxes for the receiving company and an increase in covered taxes for the distributing company.

Article 2.6 of the OECD Administrative Guidance confirms that this also includes deemed distributions.

Pushdown Limitation for Passive Income

Covered tax that relates to passive income allocated to hybrid entities or CFCs is restricted to the lower of:

- the actual amount of covered tax that relates to the passive income in the parent jurisdiction; and

- the top-up tax percentage in the subsidiary jurisdiction multiplied by the subsidiary’s passive income taxed under the CFC/hybrid regime.

This is provided by Article 4.3.3 of the OECD Model Rules.

Any remaining covered tax is allocated to the owners (eg the company with the CFC regime in place).

This ensures that the tax allocated to a CFC or hybrid entity in relation to passive income is sufficient to reach the 15% global minimum rate and does not artificially increase the covered tax of the CFC or hybrid entity (which would increase its ETR and reduce any potential top-up tax liability).

Passive income is defined as:

– dividends or similar payments;

– interest or similar payments;

– rent;

– royalty;

– annuity; or

– net gains from property that produces income listed above.

See our interactive tool to simulate the impact of the CFC pushdown limitation

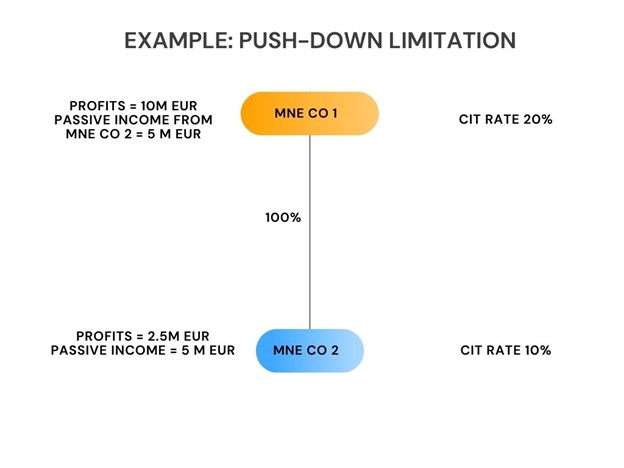

Pushdown Limitation – Example

MNECo1 is part of an MNE group subject to the Pillar Two GloBE rules. It is resident in a Country A that has a domestic corporate income tax rate of 20%.

MNECo2 is a wholly-owned subsidiary of MNECo1 and is resident in Country B, which has a corporate income tax rate of 10%.

Country A has a CFC regime which taxes the foreign passive income of MNECo2.

MNECo1 has profits of 10,000,000 euros and is additionally taxed on foreign passive income of MNECo2 of 5,000,000 euros.

MNECo2 has trading profits of 2,500,000 euros and taxable passive income of 5,000,000 euros.