General

The allocable share is defined in Article 2.2.1 of the OECD Model Rules as:

Top-Up Tax of the Low Taxed Entity x Parents Inclusion Ratio

The inclusion ratio is the:

Pillar Two GloBE Income of the Low Taxed Entity less any amount attributable to other ownership interests/Pillar Two GloBE Income of the Low Taxed Entity

This means that if the low-taxed entity is wholly owned by the parent entity, the inclusion ratio would be 100% and all of the low-taxed entity’s top-up tax would be levied on the parent under an Income Inclusion Rule (IIR).

Pillar Two GloBE Income Attributable to Other Owners

A key component of the IIR calculation is ascertaining the amount of Pillar Two GloBE income attributable to other owners. This then feeds directly into a parent entity’s allocable share, and the amount of top-up tax they are liable to pay.

The way the Pillar Two GloBE rules do this is in Article 2.2.3 of the OECD Model Rules, by deeming consolidated financial accounts to be prepared. As part of the accounting consolidation, any income or assets attributable to other non-group owners would be eliminated so that the consolidated accounts reflect just the income, expenses, assets and liabilities of the group.

In order to do this, they make a number of assumptions so that the hypothetical consolidation actually achieves the correct allocation of Pillar Two GloBE income:

1. The accounting standard used for the deemed consolidation is the same as the UPE’s consolidated financial statements.

2. The parent entity owned a controlling interest in the low-taxed entity and there is a requirement to consolidate the results of the low-taxed entity in the deemed consolidated accounts.

This is an assumption to fit the Pillar Two GloBE rules to accounting rules (even if the accounting consolidation is only hypothetical). Just because the Ultimate Parent Entity (UPE) may have to prepare consolidated accounts doesn’t mean that a parent entity would.

The parent entity may for instance hold a minority interest in the low-taxed entity even though the UPE holds a controlling interest. This would then mean there may not be a requirement for the parent entity to prepare consolidated accounts. This assumption prevents that from happening.

3. Consolidated financial accounts eliminate intra-group transactions.

However, for the purposes of the Pillar Two GloBE rules intra-group transactions are usually included (unless of course an election is made for consolidated treatment for constituent entities in the same jurisdiction. For more information on this, see the Consolidation Election).

An assumption is therefore made that all transactions are with non-group companies. This prevents the hypothetical consolidation from eliminating intra-group transactions.

4. The final assumption removes all other owners from the deemed consolidation (by treating them as non-group companies) so that the deemed consolidation focuses on the interest held by the parent entity.

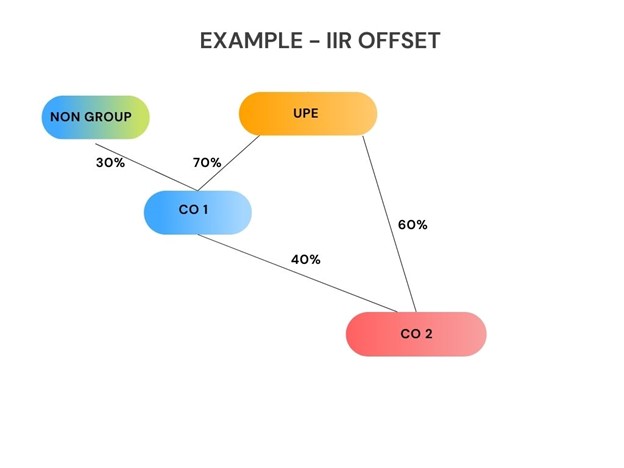

IIR Offset

Where there are two or more parent entities in a chain required to apply an IIR, a backstop mechanism applies so that the parent entity higher in the chain can reduce its top-up tax by the amount of its top-up tax levied in the intermediate holding company or POPE.

This would not apply if for instance there was a POPE that wholly-owned another POPE which in turn owned an interest in a low-taxed entity, as in this case the POPE highest in the chain has priority. But if the subsidiary POPE was not wholly-owned, both POPEs would have to apply an IIR.

This rule prevents double taxation. It could also occur where an intermediate parent entity had a non-controlling interest in another intermediate parent entity that in turn holds the ownership interest in a low-taxed entity.

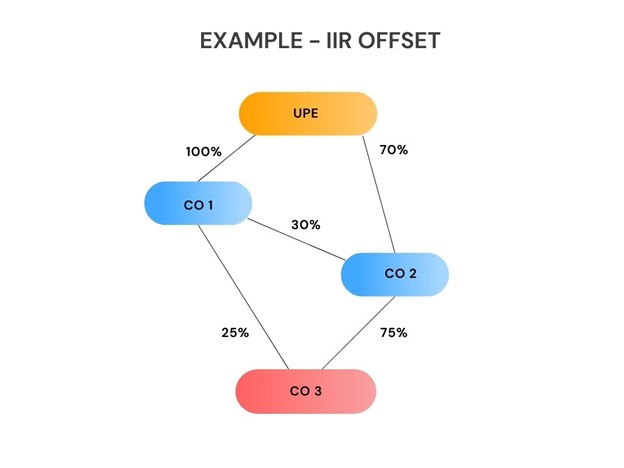

IIR Offset – Example 1

A UPE is resident in Country A. Country A does not apply an IIR.

The UPE owns 100% of Company 1 and 70% of Company 2. The remaining 30% of Company 2 is owned by Company 1. Both Companies are resident in Country B, which does apply an IIR.

Company 1 owns 25% of Company 3 and Company 2 owns 75% of Company 3. Company 3 is resident in Country C. Company 3 is a low tax entity and top-up tax of 10,000,000 euros is due under the Pillar Two GloBE rules.