Overview of Non-Tax Transparent Investment Funds

An investment entity is generally an investment fund or real estate investment fund and includes certain subsidiaries that hold assets or investments funds on the investment fund’s behalf or where substantially all of the income is dividends or losses from fair value interests or arising under the equity method of accounting. For more information, on the equity method of accounting, see excluded equity gains or losses at Pillar Two GloBE Specific Adjustments.

An investment fund is defined in Article 10 of the OECD Model Rules as an entity that:

• is designed to pool assets from a number of investors (some of which are unrelated);

• invests in accordance with a defined investment policy;

• allows investors to reduce transaction, research, and analytical costs, or to spread risk collectively;

• is primarily designed to generate investment income or gains, or protection against a particular or general event or outcome;

• investors have a right to return from the assets of the fund or income earned on those assets, based on the contributions made by those investors;

• it or its management is subject to a regulatory regime in the jurisdiction in which it is established or managed;

• it is managed by investment fund management professionals on behalf of the investors.

A key issue is that the GloBe ETR of investment entities is not subject to the general jurisdictional blending calculation, and they are treated separately. For more information on jurisdictional blending, see ETR Calculation and Top-Up Tax.

Article 7.4.2 of the OECD Model Rules provides that multiple investment entities in a jurisdiction effectively form a separate investment entity group which is subject to a separate jurisdictional ETR calculation.

The GloBE ETR calculation is similar to the standard ETR calculation, but with a twist. It is calculated as:

Adjusted Covered Taxes/MNE’s Allocable share of the GloBE Income

The allocable share of the GloBE income is based on the inclusion ratio used for the purposes of the IIR:

GloBE income of the Investment entity less amounts attributable to other owners/total GloBE income of the investment entity

The adjusted covered taxes of the investment entity are the covered taxes accrued to the investment entity based on the above inclusion ratio plus any other covered taxes that accrue to its constituent entities owners and that are pushed down to the investment entity. For more information on taxes pushed down, see Allocation of Covered Taxes.

The investment entity top-up tax calculation is then calculated in a similar way to the standard GloBE top-up tax calculation:

1. The top-up tax percentage is determined by deducting the investment entity ETR from the 15% global minimum rate

2. The MNE groups allocable share of the investment entities GloBE income is reduced by the substance-based income exclusion (‘excess profits’)

3. The top-up tax percentage is applied to the excess profits

As noted above, multiple investment entities in a jurisdiction effectively form a separate investment entity group which is subject to a separate jurisdictional ETR calculation.

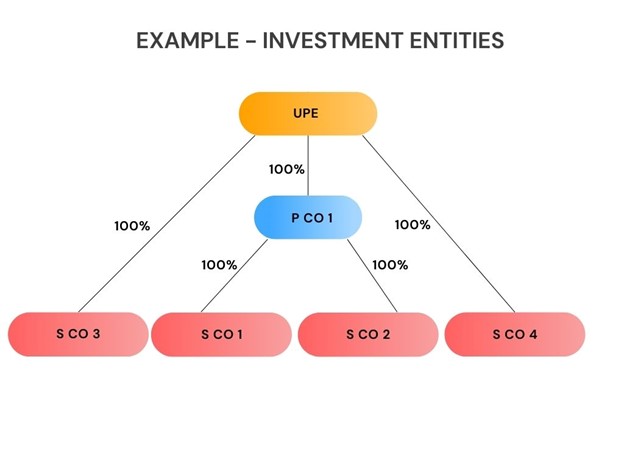

Investment Entities and Jurisdictional Blending – Example 1

The UPE is located in Country X. It owns 100% of P Co, located in Country Y. P Co owns 100% of S Co 1 and S Co 2, which are both investment entities located in Country A.

The UPE also fully owns two other constituent entities in Country A, S Co 3 and S Co 4 which aren’t investment entities.

For this example, we will keep it simple and assume there are no covered taxes pushed down to the investment entities given there are no third-party shareholders.