Belgium Issues a Circular on Pillar Two Currency Conversion

On March 17, 2026, Belgium issued a Circular on Pillar Two Currency Conversion.

On March 17, 2026, Belgium issued a Circular on Pillar Two Currency Conversion.

On March 19, 2026, Belgium issued a Consultation on the Pillar 2 IIR Top-Up Tax Return.

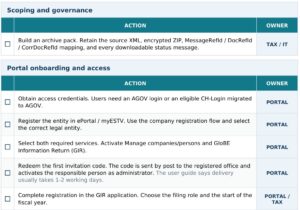

On March 19, 2026, Switzerland opened up its GIR Filing Portal. Download our Swiss GIR Filing Checklist.

On March 19, 2026, Switzerland opened up its GIR Filing Portal.

On March 10, 2026, Montenegro published its law to implement a global minimum tax (QDMTT) in its Official Gazette.

On March 17, 2026, Spain’s Navarra region published Decree 13/2026, of February 25. 2026 in its Official Gazette. This approves the Global Minimum Tax Regulations for the Navarra Region and applies to tax periods beginning on or after December 31, 2023

On March 12, 2026, Australia updated its guidance on Lodging, paying and other obligations for Pillar Two.

On March 10, 2026, Liechtenstein issued a proposal (for consultation) to amend its Minimum Tax Act to enable it to implement the January 2026 OECD Side-by-Side Tax Package.

On February 12, 2026, Finland issued a draft law to implement the OECD Side By Side Tax Package. On March 3, 2026 this was approved by the Parliamentary Finance Committee.